How we Responded Proactively…. To Deliver Performance Excellence

Business at a Glance

Sugar Business Performance Unlocking Exceptional Potential

Engineering Business Performance Looking Ahead Amid Extraordinary Challenges

Message from the chairman

Q&A with Vice Chairman and MD

Financial Review

Risk Management and Mitigation

Interactive Charts

Performance Highlights

Over the past few years, Indian sugar industry has witnessed a structural shift from a cyclical industry into more secular and consistent performance-based industry. The country, over the past few years, has witnessed consistent production much above the consumption levels, which led to a surplus scenario. This was primarily due to improved yields of sugarcane by ~25% coupled with improved recoveries of ~1.5% and the key factor that led to this improvement was change in varietal mix in the largest sugar producing state of Uttar Pradesh (UP). This surplus scenario resulted in India becoming a regular exporter of sugar in the range of 5-6 million tonnes per annum for the past two years and estimated to export 7 million tonnes in SS 2020-21. Another important factor which facilitated the structural shift is a consistent Government policy with regard to sugar and sugarcane pricing, ethanol blending programme as well as a robust export programme.

The change in varietal balance achieved across the state of UP has been phenomenal with the area under sugarcane for early and high sugar varieties going up to 90% in SS 2019-20 in comparison to an insignificant share of ~11% a decade ago. This has resulted in the state becoming the highest sugarcane and sugar producing state.

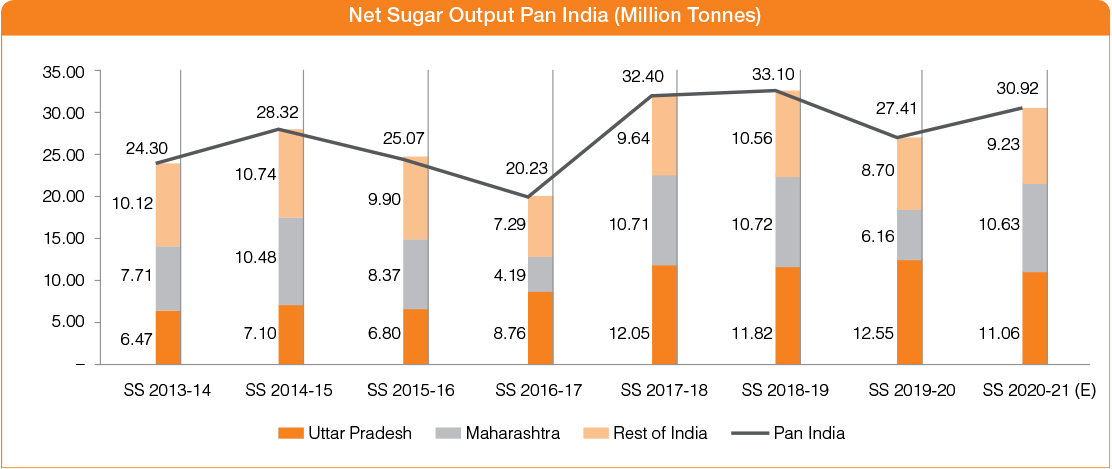

Graph showing the sugar production between UP & Maharashtra & All India trend of which amply highlights the share of UP in the all India production over the course of last eight years.

This surplus scenario resulted in India becoming a regular exporter of sugar in the range of 5-6 million tonnes per annum for the past two years and estimated to export 7 million tonnes in SS 2020-21.

India has gained a significant role in the global sugar production, being the second largest producer of sugar while it holds the first position in terms of consumption globally. Over the past four years, on account of the surplus sugar production in the country, India is also gaining its presence in the global trade.

The sugar mills in India have transformed significantly in the past decade by producing sugar, bio-electricity, bio ethanol, bio-manure and chemicals which contribute ~1.1% to the national GDP. Currently, the sugarcane and sugar related economic activities led to an annual turnover of over ₹ 1,00,000 crore.

For SS 2020-21, the sugar production in the country is expected to increase by ~13% y-o-y to 30.9 million tonnes after considering sugar diversion of about 2.14 million tonnes towards ethanol production during the year as against 27.4 million tonnes in the previous season. The annual sugar consumption of the country is around 26 million tonnes which is the highest globally. India is among the largest producers of sugar globally and it can now be categorised as a structural surplus sugar producing nation as well.

The sugar industry is one of the key strategic focus areas of the Central Government on account of its large stakeholder base as well as its role as a significant facilitator in implementing the clean energy programme for the Government. The various proactive measures by the Government have been instrumental in maintaining the sustainable performance of the industry in the recent years.

Indian Sugar Industry during COVID-19

The global economy has been impacted by the COVID-19 pandemic. The sugar industry in India has largely been safeguarded from this impact mainly on account of the Central and State Government’s proactive measures since the industry manufactures “essential goods”. The sugar industry operated without any interruption although it faced logistics challenges but these were overcome due to the active support of both the State and Central Government.

Sugar production continued even during the lockdown period of March 2020 till May 2020. Though the overall sugar off-take was lower during the April 2020 and initial days of May 2020, it later picked up due to rise in institutional demand as the manufacturing activities opened up and consumer demand rose. The sugar exports were impacted for a brief period and significant quantity was stuck at the ports but by the end of the first quarter of the financial year, exports also resumed at full momentum.

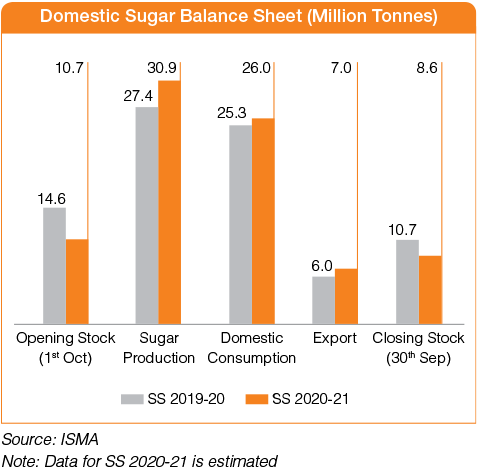

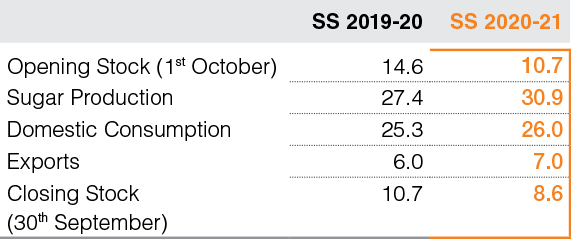

Domestic Sugar Balance sheet

For SS 2020-21, the sugar production is estimated to be around 30.92 million tonnes with a likely diversion of over 2.14 million tonnes for ethanol production. In the previous season of SS 2019-20, the sugar production stood at ~ 27.41 million tonnes and 0.8 million tonnes was diverted for ethanol production.

Sugar production estimates for UP are about 11.06 million tonnes in SS 2020-21 as against 12.55 million tonnes produced in SS 2019-20. The lower estimates in sugar production in UP are reportedly on account of lower sugarcane yields and lower sugar recoveries due to climatic factors and higher diversion to gur/khandsari units as well as through B-heavy molasses for ethanol production. Further, during the current season, it is estimated that approx. 0.73 million tonnes of sugar will be diverted for production of ethanol using B-heavy molasses and sugarcane juice, which is an increase of 78% over the previous season.

Maharashtra has produced about 70% more sugar than the previous season at 10.63 million tonnes while Karnataka has produced 4.17 million tonnes of sugar as compared to 3.38 million tonnes last season.

India started its SS 2020-21 (October to September) with an opening inventory of 10.7 million tonnes as on October 1, 2020. As on 30th June, the actual production of sugar stood at 30.66 million tonnes. Only 5 sugar mills were still operational in the country. With the opening stock of 10.7 million tonnes, the total sugar availability in the country for SS 2020-21 is estimated at 41.6 million tonnes. The sugar consumption is estimated at 26 million tonnes and with expected exports of around 7 million tonnes, thus the total offtake during the season is estimated to be around 33 million tonnes which will lead to the estimated closing inventory of sugar at 8.6 million tonnes on September 30, 2021.

For SS 2020-21, the sugar production is estimated to be around 30.92 million tonnes with a likely diversion of over 2.14 million tonnes for ethanol production.

Domestic Sugar Balance Sheet (Million Tonnes)

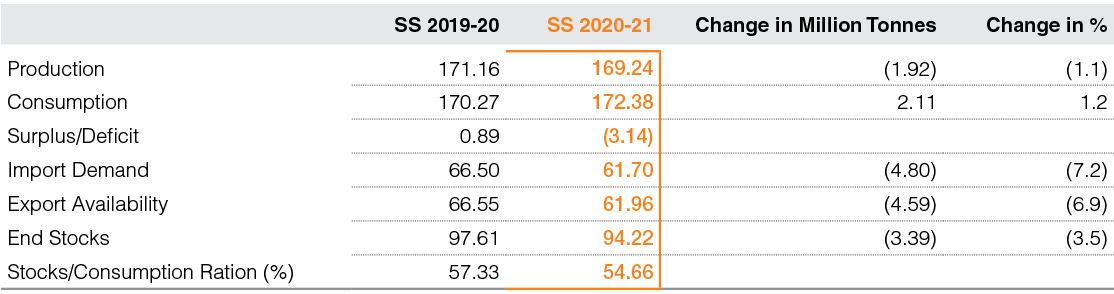

Global Sugar Balance sheet

The world sugar market is extremely volatile and is affected by the sugar policies of the key sugar producing countries notably Brazil, Thailand and India. The demand-supply dynamics in the global market is impacted by the production in these three key countries and thus affect the global sugar prices and the trading price levels.

As per recent global reports (International Sugar Organisation (ISO)), the global deficit forecast has been lowered for 2020-21 from 4.8 million tonnes earlier to 3.1 million tonnes. The World output is also expected to fall by 1.92 million tonnes in the current year. Due to the pandemic, the consumption should also reduce to 172.4 million tonnes down from 173.8 million tonnes previously forecasted but still up 1.2% year-on-year.

As per reports, the major sugarcane producing region in Brazil, Centre-South Brazil, completed the 2020-21 (April/March) harvest with 605.46 million tonnes of sugarcane crushing which is an increase of 2.6% over the 590.36 million tonnes crushed in 2019-20 as per the industry data. The Centre South (CS) region of Brazil processed 46.07% of total raw material into sugar during the 2020-2021 harvest producing 38.46 million tonnes of the sugar, representing a 43.73% increase over 26.76 million tonnes in the previous cycle.

As on Jun 29, 2021, reports indicated that sugar production estimates for Brazil’s CS region’s 2021-22 were revised downwards to 34.1 million tonnes from an April projection of 35.6 million tonnes, as persistent dry weather hurt cane development, food trader and supply chain services. It was also reported that Brazilian millers will be able to crush only 535 million tonnes of sugarcane this season, down from earlier estimates of 558 million tonnes. The update estimates for sugarcane crush are the lowest since 2012.

In Thailand, according to industry reports, the sugarcane crop in Thailand in 2020-21 suffered from unfavourable weather conditions again leading to decline in sugar production to 7.6 million tonnes as against 8.27 million tonnes in 2019-20. Higher local cane prices and forecasts of ample rains suggest a production recovery in Thailand for 2021-22 to be about 10.5 million tonnes, up 38% year-on-year.

Global Sugar Balance Sheet (Million Tonnes)

Government Policies

In order to support the dynamics of the sugar market and ensure timely payments to the farmers, the Central Government announced various measures during the current season:

- An export quota of 6.0 million tonnes was allocated to all sugar mills on December 31, 2020 with export date till September 30, 2021 and notified scheme for providing assistance to the sugar mills for expense on marketing costs including handling, upgrading and other processing costs and costs of international and internal transport and freight charges on export of sugar. The aggregate assistance under this scheme was prescribed at ₹ 6,000 per tonne of exports to be used to clear cane payment dues of farmers.

- Fixed Remunerative Price (FRP) of sugarcane for SS 2020-21 was increased by ₹ 10/quintal to ₹ 285/ quintal calculated at 10% recovery with a premium of ₹ 2.85 per quintal for every 0.1% rise in recovery.

- Minimum Selling Price (MSP) fixed by the Government in Feb 2020 at ₹ 31/kg remained unchanged.

- The Government of UP kept the sugarcane prices at the same level as last year for the current SS 2020-21. The State Advised Price (SAP) remained at ₹ 315 per quintal for the common variety, while the prices for early variety and rejected varieties of sugarcane remained at ₹ 325 and ₹ 310 per quintal, respectively.

- The release quota mechanism set up by the Government in the last season is also continued during the current season so as to regulate the supply of sugar into the market, thereby enabling steady sugar prices in the market.

- Later on May 20, 2021, the Government announced a reduction in its assistance to the export of sugar from ₹ 6,000 per tonne to ₹ 4,000 per tonne of sugar against MAEQ for SS 2020-21 owing to global market dynamics. The reduced assistance is be applicable for the quantity of Maximum Admissible Export Quantity (MAEQ) for which the export contracts/agreements are signed on or after May 20, 2021

Sugarcane Prices

The Central Government announced Fair & Remunerative Price (FRP) for sugarcane and for SS 2020-21 was increased by ₹ 100 per tonne at ₹ 2,850 per tonne as per guidelines of Commission for Agricultural Costs and Prices (CACP).

The Government of UP kept the sugarcane prices at the same level as last year for the current SS 2020-21, the State Advised Price (SAP) remained at ₹ 315 per quintal for the common variety, while the prices for early variety and rejected varieties of sugarcane remained at ₹ 325 and ₹ 310 per quintal, respectively.

Sugarcane pricing plays a significant factor in the competitiveness of Indian industry. In view of high sugarcane cost and the resultant higher cost of production of sugar, it is not possible to compete with the export prices without any support from the Government. Sugarcane price in India is 70- 80% higher than that of Brazil or Thailand. For self-sufficiency, sugarcane pricing policies would need rationalisation and these need to be brought in tune with global practices. In the state of UP, sugarcane arrears as on May 31, 2021 stood at ₹ 11,803 crore. The Maharashtra sugarcane arrears based on FRP excluding Harvest & Transport (H&T) stood at ₹ 957 crore as on June 15, 2021.

The mismatch between sugar prices and cane prices adversely affects the liquidity of mills and their ability to pay the sugarcane price to sugarcane farmers. The sugarcane farmers and sugar mills are hopeful of an early announcement by the Government regarding increase in MSP of sugar as a measure to improve revenue realisation by mills and payment to farmers, which will in turn ease the current situation of very high sugarcane price arrears.

Sugar Exports

On the export front, Indian millers had achieved export programme for SS 2019-20 and the country exported 6 million tonnes, even though exports were impacted due to lockdown and other logistics problems. Similarly, sugar industry has responded well to SS 2020-21 export programme, even though it was announced late in Dec 2020 after the commencement of the SS 2020-21. Strong international prices helped Indian sugar industry to contract significant quantity of sugar in a short span of time. Market reports are encouraging and indicate that, as on June 15, 2021, contracts of ~5.8 million tonnes have already been made so far out of 6 million tonnes for the current season prescribed by the Central Government. It is also estimated that physical exports of almost 4.4 – 4.5 million tonnes of sugar have been completed during January 2021 to May 2021. In view of strong international prices, sugar may be exported even beyond export quota of 6 million tonne under Open General Licence (OGL) without availing any export assistance from the Government to maintain liquidity of funds and to generate adequate funds to be able to pay the full cane price to sugarcane farmers. It is possible that export quota may even be surpassed by up to one million tonne, including spill over from the previous season export quota. Expected substantial exports will help in correcting the surplus sugar inventories.

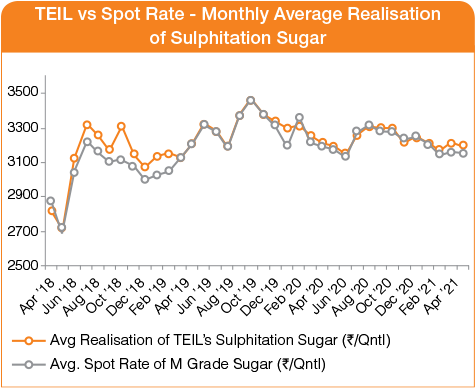

Sugar Prices

Domestic

The average sugar prices for the industry remained range bound during SS 2020-21 with a peak reaching ₹ 3,300 per quintal from a bottom of ₹ 3,100 per quintal. This is mainly on account of the size of the release quota allocated to the domestic mills and brief impact of the lockdown. The carryover stocks of previous season combined with the stocks of SS 2020-21 led to higher inventory in North Indian states. This led to a variation in the domestic price realisation.

Further, the opening stock of 10.7 million tonnes at the start of the season, which is sufficient for more than 5 months’ consumption as against the ideal stock equivalent of 2-2.5 months’ consumption, also impacted the prices during the crushing season. Additionally, expected substantial increase in sugar production in the state, led many sugar mills from Maharashtra to sell in those markets that are traditionally catered by UP sugar mills. These sporadic sales were to alleviate the problem of storage of sugar and to improve their working capital, thereby putting pressure on the overall market prices.

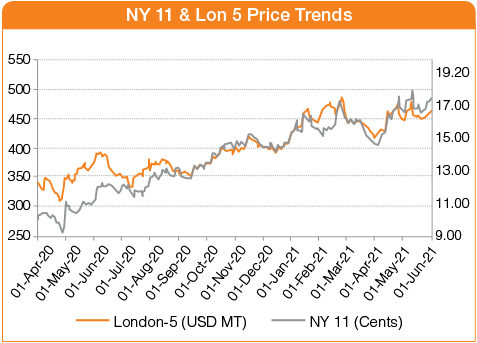

Global

In the last financial year, the global sugar prices remained at lower levels during the beginning of the year from April to May 2020 due to lockdown impacting the overall demand in various parts of the world. The prices started moving upwards from Sep 2020 with rising demand owing to ending of the lockdowns.

The lower production estimates from Thailand and higher diversion of sugar towards ethanol in India led to further firming of prices from September to December 2020. The prices further increased from January 2021 to February 2021 due to reports of dry conditions in Brazil and increasing energy prices and remained range bound since March 2021.

In view of estimated significantly lower production in Brazil in 2021-22, the supply may continue to be tight until Jan 2022 when supply of Thai sugar of 2021-22, which is expected to bounce back to over 10 million tonnes, starts entering the market. Until then, firm international sugar prices may be maintained. It may provide a window for the Indian sugar to export at remunerative prices.

The average sugar prices for the industry remained range bound during FY 21 with a peak reaching ₹ 3,300 per quintal from a bottom of ₹ 3,100 per quintal.

Q&A with Vice Chairman and MD

Q&A with Vice Chairman and MD

2021 Triveni Engineering, All Rights Reserved